.avif)

Companies around the EU are adjusting to a new era of sustainability reporting. As of July 2023, the European Commission adopted the European Sustainability Reporting Standards (ESRS), 12 sustainability reporting standards across environmental, social, and governance issues. The ESRS implement the requirements of the Corporate Sustainability Reporting Directive (CSRD).

The ESRS standardise sustainability reporting in the EU and integrates sustainability into corporate strategy. Promoting transparency for stakeholders and consumers, the ESRS will help hold companies accountable to the EU’s goals for climate neutrality by 2050 and the transition to a more just and sustainable economy. Large companies previously subject to the Non-financial Reporting Directive are the first in line for the CSRD and must report in 2025 on the financial year 2024. Over the following years, thousands of other companies will come into scope, with all listed SMEs in the EU needing to comply by 2028 at the latest.

The ESRS take time to understand, much less implement. After all, the published standards are nearly 300 pages long and mandate reporting on dozens of data points throughout the value chain. This means that if your company must comply, there’s no time to waste in getting up to speed on the standards — especially if your company operates in complex supply chains.

In this article, we’ll explore the most important things directors need to understand about the ESRS and key steps to compliance. We’ll also consider the role of supply chain traceability tools in robust sustainability reporting.

What are the European Sustainability Reporting Standards?

If the CSRD is like a blueprint for sustainability reporting — laying out the vision, principles, and objectives for building — the ESRS are like the detailed building plans that identify the materials, measurements, and processes needed to get the job done.

Although they are interconnected, the CSRD and ESRS play separate roles. Providing the necessary framework to implement the CSRD, the European Sustainability Reporting Standards are a set of detailed guidelines for reporting across environmental, social and governance topics within the company.

The ESRS has 12 reporting standards in total:

- Two “cross-cutting” standards or broad standards all companies must include in their reporting, and

- 10 topical standards subject to the outcome of a materiality assessment

The European Financial Reporting Advisory Group (EFRAG), which advises the European Commission, developed the standards and published supporting guidance to help companies with implementation. EFRAG is currently developing sector-specific and SME-proportionate standards, initially expected to be ready at the end of June 2024. However, this has been pushed back to 2026.

ESRS Standards: A breakdown of the categories

To better understand the standards and what they cover, let’s look at each of the five major categories. We’ll start with the two mandatory cross-cutting standards, which apply broadly across multiple areas of sustainability reporting, and then move on to the three topical areas. These standards provide overarching principles and requirements that ensure consistency, comparability, and reliability across all sustainability disclosures, regardless of the industry or specific sustainability issue being reported.

ESRS 1: General requirements

The first of two cross-cutting standards, ESRS 1 lays out the key concepts and requirements of the reporting framework. This standard outlines the reporting areas, what information is required in reporting, the role of due diligence throughout the process, and time horizons. This standard is also where you can find concepts foundational to the ESRS, such as:

- The scope of the “value chain”: the activities, resources, and relationships in the company’s own operations, along its supply and distribution channels, and throughout the broader environment in which the company operates

- The double materiality concept as the basis of sustainability disclosure: how companies need to consider sustainability reporting from both a financial and impact materiality perspective

- The importance of stakeholder engagement: ‘affected stakeholders” and “users of sustainability statements,” which encompass everyone in the value chain and who need to be consulted throughout the reporting process

ESRS 2: General disclosures

The second cross-cutting standard within the framework details the disclosures all companies must include in their sustainability reporting, regardless of the outcome of a double materiality assessment.

ESRS 2 explains the four-pillar reporting approach companies must use while reporting sustainability information across all topical areas. These four pillars are:

- Governance to disclose the administrative, management, and supervisory bodies of a company, and their involvement and expertise in managing sustainability issues

- Strategy to disclose the company’s overall strategy relating to sustainability matters, its business model and value chain, and how companies engage with stakeholders

- Impact, risk and opportunity management to disclose the company’s process of identifying impacts, risks and opportunities and the results of its materiality assessment

- Metrics and targets to disclose targets a company has set, metrics to report, and how they are tracking the effectiveness of their actions

ESRS 2 includes a list of data points that must be reported regardless of the outcome of the double materiality assessment, which EFRAG have published in a supporting document. It also includes a list of “minimum disclosure requirements” that must be reported for every material topic. Additionally, companies must use the materiality assessment to identify more detailed information that must be reported for material topics.

E1 to E5: Environmental standards

The environmental standards are the first topical category included in the ESRS. While climate change reporting is a large part of the environmental standards, it is just one area. Companies must also report on topics like pollution and biodiversity. The five environmental standards require disclosures in these areas:

- ESRS E1 Climate change: The development of a climate transition plan and related information, such as greenhouse gas, energy consumption, and climate adaptation.

- ESRS E2 Pollution: Information relating to water, air, and soil, as well as other substances of concern.

- ESRS E3 Water and marine resources: Information relating to water consumption and their impacts on marine resources, like ocean degradation.

- ESRS E4 Biodiversity and ecosystems: Information relating to biodiversity and the impact on ecosystems.

- ESRS E5 Circular economy: Information relating to resource use — specifically the inflows and outflows of resources – and how the company plans to minimise waste while maintaining product and material value.

Companies are required to assess each topic in a double materiality assessment and provide justification as to whether it material or immaterial to the company. This determines whether the topic requires detailed reporting. From there, each topic has a set of minimum disclosures a company must include in reporting for material topics, and additional information that is necessary to report depending on the relevance of that information.

For example, if an automotive company determines that circular economy is a material topic, the company would need to report on any policies and targets they have set related to resource use. They would also potentially need to report on data points like the total weight of products and materials used, the percentage of biofuels used for non-energy purposes, and other more detailed disclosures5.

It is worth noting that the ESRS E1 standard on climate change differs from the other topical standards. If a company decides it is immaterial to their reporting, they must then provide extra justification and a forward-looking statement about this topic. This makes it more difficult, in practice, for companies to avoid reporting on climate change.

S1 to S4: Social standards

The next category of standards, S1 to S4, covers social standards throughout the value chain. Overall, these standards aim to increase transparency around human rights and worker well-being. Specifically, the standards require disclosures in these areas:

- ESRS S1 Own workforce: Information relating to a company’s own workers, including worker engagement, wages, social protection, and employees’ overall health and well-being.

- ESRS S2 Workers in the value chain: Information relating to policies, processes, and due diligence measures for workers throughout their entire value chain.

- ESRS S3 Affected communities: Information relating to affected communities, for example, the economic, cultural, and political rights of communities, as well as particular rights of indigenous peoples.

- ESRS S4 Consumers and end-users: Information relating to consumers and other end-users in the value chain in terms of stakeholder engagement, privacy, freedom of expression, personal safety, and social inclusion

Like the environmental standards, social standard topics are also subject to the double materiality assessment. Companies must disclose how each topic was deemed as material or immaterial, and disclose minimum data points for any topics deemed material. Other more granular information may need to be reported based on the assessment. For example, if an electronics company determines that consumers and end-users is a material topic, they would potentially need to disclose data points such as severe incidents that have occurred related to consumers and end-users and how they are mitigating risks.

G1: Governance standard

The third topical category is governance, with only one standard in this category detailing business conduct reporting requirements. This standard requires disclosures relating to:

- Corporate culture

- Business conduct policies

- Management of relationships with suppliers

- Bribery

- Political influence

- Payment practices, especially with SMEs

As an example, an aviation company that determines that this standard is material would potentially need to report on points like policies related to whistleblower protection, payment policies, and policies on anti-corruption and anti-bribery.

Steps to comply with the ESRS Standards

Considering how comprehensive these standards are and the relatively short window to comply, where should companies begin with CSRD and ESRS preparations? Let’s break down the process into five big steps.

Step 1: Understand the ESRS requirements

The first step is understanding the scope of the requirements and their implications. It’s crucial to take time to familiarise yourself with the standards so you can consider what it means for your company. And of course, the reporting process will be slightly different for each organisation. It’s helpful to read through the ESRS standards themselves, as well as consult the additional materials from EFRAG that summarise key implementation advice and guidance on:

- The materiality assessment

- Value chain

- ESRS data points

While you do want to have a working understanding of the requirements yourself, working with a sustainability consultant to understand the standards and implications for your company will save precious time and ensure you don’t miss critical aspects of the process.

Step 2: Establish responsibilities and conduct the double materiality assessment

Once you have a deeper understanding of the standards, the next step will be to establish and delegate responsibilities throughout the team. Other than the sustainability department, close collaboration with finance and legal teams, as well as departments including human resources, communications, and procurement, will be required. Training your staff In order to embed sustainability reporting knowledge throughout each department, training your stuff will be essential.

An early project you will need to tackle is planning your stakeholder engagement process and conducting the double materiality assessment as the basis for your reporting needs. EFRAG has published guidance on this assessment, but you can also design a process that works best for you company.

Step 3: Develop robust data collection and management systems

The outcome of the materiality assessment will allow you to audit your sustainability data reporting systems and your reporting needs. The assessment might reveal, for instance, that you have clear visibility into your own operations but need much more data from your suppliers.

Working with supply chain traceability partners like Circularise can fill the gaps, providing you with more granular data and a more complete picture of your entire value chain. Supply chain traceability tools and robust data collection will support compliance with not just the ESRS, but many other international standards and laws, such as the Corporate Sustainability Due Diligence Directive, the EU Battery Regulation, RED II regulations for biofuels, and many others.

Step 4: Measure sustainability performance against targets and standards

Another aspect of preparing your reporting is setting and disclosing time-bound, outcome-oriented targets for each topic. For instance, when disclosing your climate transition plan as part of ESRS E1 on climate change, you will need to disclose greenhouse gas emission reduction targets across scopes 1, 2, and 3 for at least 2030 and 2050. Additionally, you should demonstrate the methods you're using to monitor these targets to evaluate the effectiveness of your actions.

You will find many overlaps between the targets you need to report as part of the ESRS and other international standards like the International Sustainability Standards Board (ISSB) and the Global Reporting Initiative (GRI), since EFRAG collaborated closely with both.

One of the more important sets of targets you will need to report relates to the climate transition plan as part of ESRS E1: climate change. This standard requires you to consider various climate scenarios, set and report GHG emission reduction targets for at least 2030 and 2050, and disclose how you are measuring progress.

Step 5: Prepare reporting and engage third-party auditors for verification

The final stage of compliance will involve preparing and integrating this information into your annual management report. The management report should include:

- Analysis of development and performance of the company

- Descriptions of key risks and opportunities

- Likely future developments of the company

- Corporate governance statement

- A sustainability statement including detailed reporting on general disclosures and topical standards

To verify the information in the sustainability statement, you will need to engage an external assurance provider, just as you would with financial information.

Overall, while the ESRS holds companies to a high reporting standard, no company will be able to manage “perfect” data or sustainability performance in the first year of reporting. Instead, think of it as an iterative process. With each year of sustainability reporting, you’ll be able to move toward more visibility and transparency, which will in turn equip leadership in the company to make better decisions.

The role of supply chain traceability in the ESRS Reporting Standards

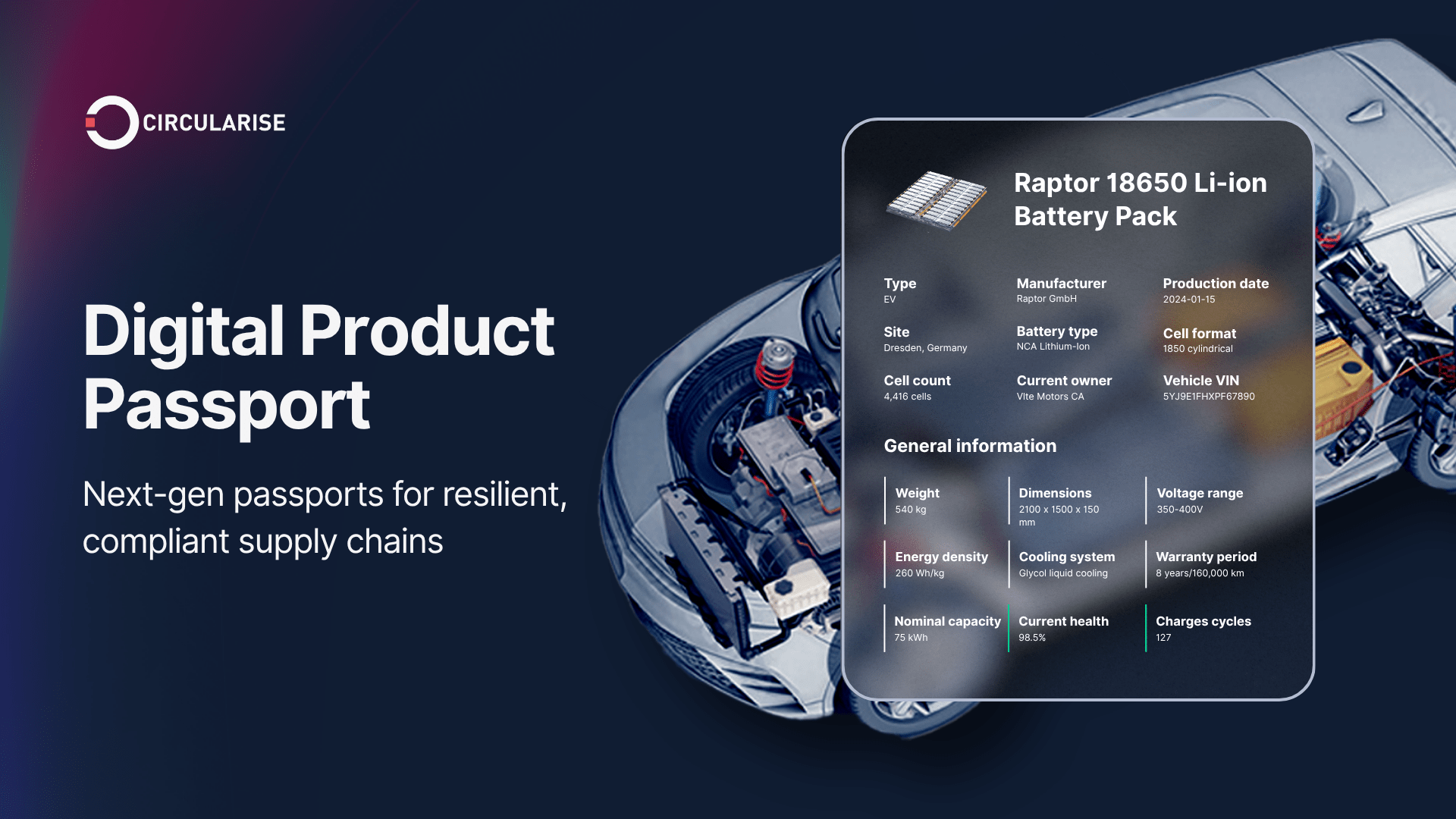

For many companies, especially those in complex industries like electronics and metals, supply chain traceability is a key ingredient for understanding and reporting risks, impacts, and opportunities throughout the value chain. Traceability tools like Circularise’s digital product passports and MassBalancer provide granular data into your supply chain for reporting without compromising confidential data.

Circularise has partnered with forward-thinking companies and consortiums to collect more granular data across value chains. With the Porsche project, Circularise digitised materials within their own operations and those of Tier 1-2 suppliers on the blockchain, allowing the company to effectively track and reduce their environmental impact.

In another example, Circularise has been working with multiple partners on a Circular System for Assessing Rare Earth Sustainability (CSyARES). This project focuses on researching and developing a block-chain traceability system to support the needs and standards of the rare earth elements industry, starting with digitising the Rare Earth Industry Association’s (REIA) sustainable mining standards. The project involves integrations to collect and communicate life cycle assessment data throughout the supply chain.

The applications of this supply chain traceability technology go beyond compliance. The decentralised blockchain technology enables companies to collect, track, and manage information to become industry leaders in the circular economy.

Conclusion

Together with CS3D and CSRD, the ESRS are raising the bar for sustainability reporting for large companies active in the EU. Sustainability reporting is no longer a “nice-to-have” exercise, but a process that’s as crucial as financial reporting for a company’s long-term success. With the largest companies already in scope, now is the time to begin preparations if you have not yet begun. Aligning teams, especially sustainability, finance, and legal will be essential, and starting the double materiality assessment process will help you assess the next steps.

In particular, larger and more complex companies will need to audit the traceability solutions and reporting they have in place and decide whether they need a more robust solution. Partnering with sustainability consultants and traceability experts like Circularise will equip you with confidence you need to move forward, and the granular level of data you need to fulfil your compliance requirements.

Circularise is the leading software platform that provides end-to-end traceability for complex industrial supply chains. We offer two traceability solutions: MassBalancer to automate mass balance bookkeeping and Digital Product Passports for end-to-end batch traceability.

Learn how Circularise’s supply chain traceability platform can help you with ESRS and CSRD compliance, get in touch with the Circularise team today.