.avif)

Update: Please note that 2025 updates under the EU Omnibus Regulation may affect certain requirements and timelines. Readers are advised to review the latest Omnibus developments for the most up-to-date context.

It’s official — as of May 2024, the European Union has not one, but two mandatory sustainability directives in place with a far-reaching, global impact.

As part of the European Green Deal, the Corporate Sustainability Reporting Directive (CSRD) is already in effect, with the first wave of companies needing to comply from January 2024. The EU Council have also approved the Corporate Sustainability Due Diligence Directive (CSDDD, or CS3D) as of May 2024, with deadlines starting in 2027. These directives come on top of many other legislations and frameworks on sector and topic-specific issues.

The good news is that the CSRD and CS3D complement one another. They’re both critical building blocks of the EU Green Deal, giving companies the frameworks and guidance necessary to become climate-neutral by 2050 and enable a just transition.

Both integrate international frameworks and standards such as the UN Guiding Principles on Human Rights and the OECD Guidelines for Multinational Enterprises, ensuring consistency across these international standards.

At the same time, each directive fulfils a specific need in facilitating the green transition. In this article, we’ll explore the key differences between the two directives, share guidance on preparation, and provide a unique perspective on how traceability solutions can help your company comply more easily with these directives.

What are the CSRD and CS3D?

First, let’s understand the distinct scope and purpose of these two directives within EU sustainability legislation. As their names imply, the CSRD primarily focuses on reporting sustainability information, while the CS3D focuses on taking action through due diligence procedures.

The CSRD

The Corporate Sustainability Reporting Directive or CSRD requires in-scope companies to include comprehensive sustainability information as part of their regular financial reporting. Replacing and expanding on the Non-financial Reporting Directive (NFRD), the aim of the CSRD is to foster transparency in sustainability practices, providing investors and customers a more holistic view of the health and future performance of the company.

The CSRD and the supporting European Sustainability Reporting Standards introduce expanded legal requirements and a “double materiality” framework for reporting across impacts, opportunities, and risks across the three overarching areas of the environment, social, and governance.

The CSDDD or CS3D

The Corporate Sustainability Due Diligence Directive, also known as the CSDDD or CS3D, requires in-scope companies to implement due diligence procedures throughout their supply chain. According to this directive, companies need to work closely with suppliers and stakeholders to identify and mitigate potential risks throughout their chain of activities. Companies must also implement comprehensive due diligence policies that address these risks, monitor implementation, and do what they can to remediate negative impacts if and when they do occur.

CSRD vs CSDDD: The key differences

While complementary, the CSRD and CSDDD have significant differences in terms of overall scope, timeline, and the type and size of companies they affect.

Reporting requirements vs Due diligence mechanism

The key difference in focus between the two directives is that one focuses on reporting requirements, while the other focuses on due diligence. This difference in focus has distinct implications for directors as they consider their duties.

The CSRD mandates reporting and transparency within the supply chain. It legally requires in-scope companies to comply with the detailed European Sustainability Reporting Standards, giving stakeholders a thorough understanding of the company’s activities and preventing greenwashing. Directors must establish ESG policies, integrate environmental and social policies into their overall strategy, and conduct comprehensive reporting to facilitate transparency and accountability.

The CSDDD, on the other hand, focuses on risk mitigation and response through due diligence, ensuring that companies are taking action to prevent and address risks in the supply chain. According to CS3D, directors must consider the impacts of their business on human rights and the environment and implement due diligence processes aligned with the OECD Guidelines for Multinational Companies. This due diligence focus provides the legal mechanism for governments to ensure companies are not simply reporting on sustainability performance, but also taking action toward climate neutrality, fair labour, and the responsible use of resources.

Reporting vs Annual statement

To integrate sustainability information into corporate financial reporting, the CSRD requires companies to include sustainability data and assessments in their annual management reports.

The formatting of this information should comply with European Single Electronic Format (ESEF) standards, which specify an XHTML format using XBRL markup, or digital tagging. The management report must consider sustainability factors in its analysis and include a comprehensive sustainability statement according to the European Sustainability Reporting Standards. Companies will have to submit their reports to the European Single Access Point, which is expected to open in the summer of 2027. The CS3D does not introduce new reporting requirements, since other policies like the CSRD are quite comprehensive on these points. Instead, to demonstrate compliance, the CS3D requires companies to publish on their website an annual statement on due diligence procedures and developments. Companies will also need to submit this statement to the European Single Access Point after it becomes available.

CSRD mandates reporting on financial risk and opportunity

Another key difference between the directives is that the CSRD emphasises the “double materiality” approach, which means that companies must report on both financial materiality and impact materiality.

Financial materiality covers how sustainable topics like resource use and climate change will affect the financial health of the company. Impact materiality, in contrast, refers to how the company’s activities affect stakeholders and the broader environment. The CSRD incorporates both these perspectives to integrate sustainability and financial concerns. This means the CSRD will require close collaboration between sustainability and finance departments.

The CS3D primarily addresses impact materiality by requiring due diligence measures to reduce impacts on employees, communities, and the environment. While finance departments will still be involved in ensuring teams have the resources they need to comply with the directive, they will not be as involved on CS3D implementation.

CS3D will have greater impact on procurement teams

The CS3D will have a greater impact on procurement teams than the CSRD, since a critical aspect of this directive is supplier due diligence. As part of the CS3D, procurement teams must review supplier practices and ensure adherence to the directive. This includes SME business partners, which the directive defines as micro, small, or mid-sized companies not part of a large group.

Procurement can’t simply pass the burden of compliance onto their SME suppliers, or discriminate against SMEs that may already be struggling with financial and administrative issues. Instead, the CSDDD encourages companies to support their SME business partners with due diligence resources and implementation.

Whether their suppliers are large or small enterprises, procurement and legal teams of in-scope companies will need to work closely together to review and set up purchasing, contracts, and collaboration strategies that are in line with CSDDD requirements.

CSRD’s “value chain” is broader than the CSDDD’s “chain of activities”

The CSRD has a broader scope that covers the entire “value chain,” while the CSDDD covers a narrower “chain of activities” of a company. This may seem like a subtle difference in wording, but the terms have big implications.

CSRD’s “value chain” includes all activities related to the creation, delivery, and support of a company’s products and services. This includes virtually all business relationships a company might have, and all internal operations, upstream activities, and downstream activities, from raw material extraction to a product’s end-of-life.

CS3D’s “chain of activities” is also broad, but it focuses on the activities of a company and the company’s suppliers. This narrower scope covers upstream activities from a company’s business partners and downstream activities in distribution, transport, and storage of the product, but not product disposal.

CS3D has no materiality threshold

The CSRD may have broader overall coverage than the CS3D due to the value chain concept, but in practice companies may be able to exclude some activities from their reporting. This is because the directive allows companies to use a “materiality threshold” to determine some of the activities it includes in the sustainability report. A company may be able to exclude a topic from reporting as long as the topic is not one of the mandatory data points as part of the “cross-cutting standards,” or the topic is genuinely “immaterial” according to the company’s double materiality assessment.

The CS3D, in contrast, has no materiality threshold. According to the directive, a company must assess and implement due diligence measures across all relevant activities. Companies will still prioritise activities and impacts to establish a proportional response based on the severity and likelihood of the impact. But a company will need to take measures to prevent less likely and less severe impacts from happening, even if they do not reach the materiality threshold of the company’s Double Materiality Assessment.

More companies are in scope for the CSRD than the CSDDD

Another important difference is that the CSRD applies to a much greater number of companies compared to the CSDDD: approximately 50,000 vs 5,500. From January 2026, the CSRD will apply to all listed SMEs whose assets are traded on EU financial markets, with the very last wave of companies having to report no later than 2028.

The CSDDD, on the other hand, applies to a smaller number of large EU and non-EU companies, primarily those with at least 1,000+ employees and 450 mil+ euro turnover — an estimated total of 5,500 companies. However, the CSDDD will still have a large impact, since the directive also impacts suppliers of these in-scope companies.

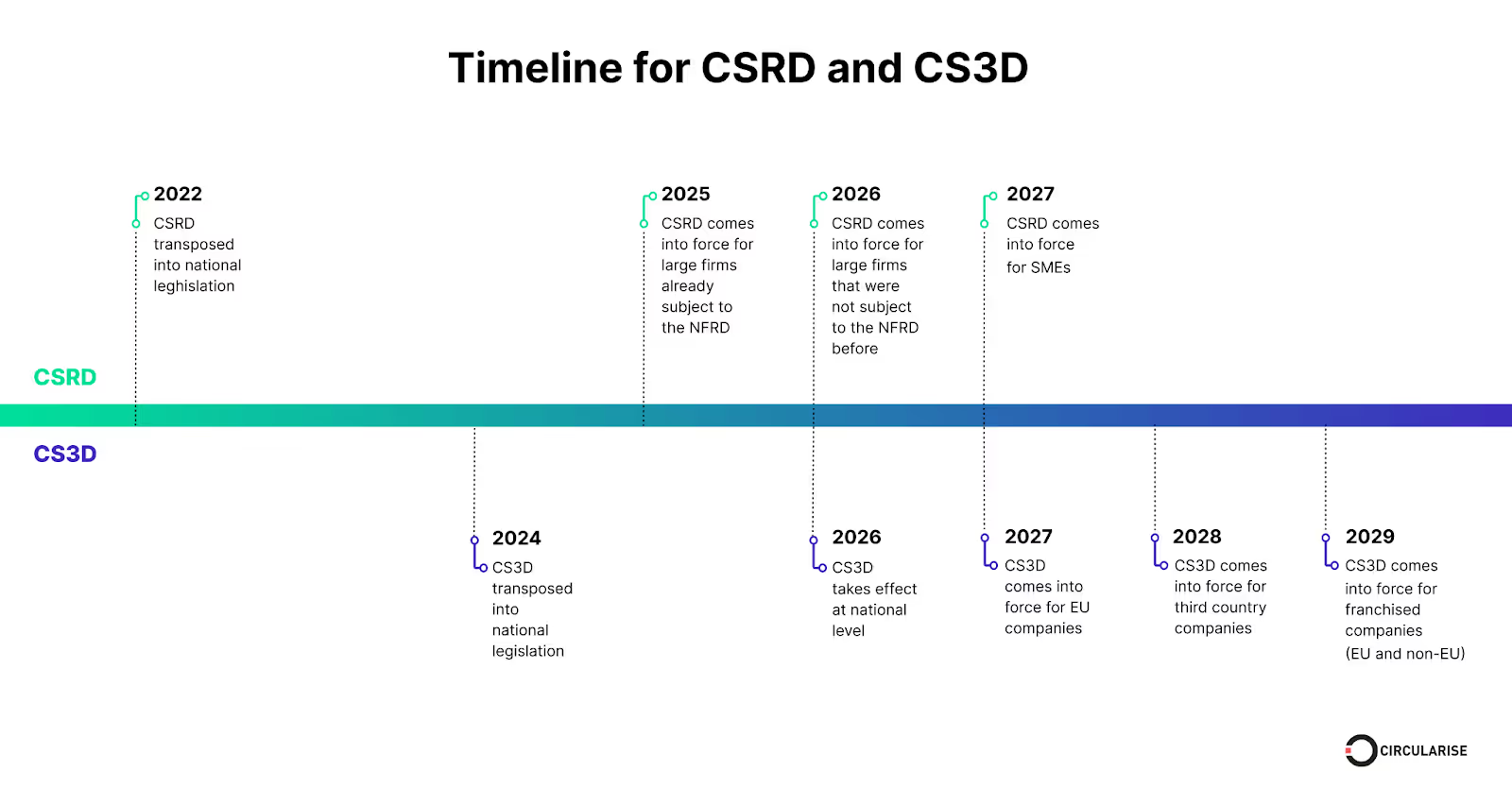

CSRD has earlier rollout

The two directives follow distinct timelines, with the CSRD rolling out ahead of the CS3D. In 2024, the CSRD came into effect for companies that were already subject to the NFRD. Specifically, this first group is large public-interest entities meeting at least two of the three criteria

- 500+ employees

- 40M EUR net turnover

- 20M EUR in assets

These companies must file their reports in 2025 for the 2024 financial year, with other companies coming into scope in 2026 and 2027.

The CS3D has a later timeline. From 2027, the first wave of companies — those with 5,000+ employees and 1,500 million euro turnover in the EU — must comply. Other companies will come into scope in 2028 and 2029.

Preparing for CSRD and CS3D compliance

How should companies prepare for sustainability compliance, given that the two directives overlap? Here are several considerations and examples from corporations that are already on their journey to compliance.

Similarities in preparation for CSRD and CSDDD

Due to the overlap and intersecting concerns of the two directives, there are a number of similarities in how companies will need to prepare for them. To highlight the top factors:

- Strategy and implementation of both directives must be coordinated: Many of the preparation duties such as overall strategy, risk assessments, hiring, vetting vendors and authorities will overlap. This means that companies subject to both directives must ensure their legal, sustainability, finance, procurement, and hiring teams are coordinating the many moving parts of compliance with both directives.

- Climate transition plans: Both directives require in-scope companies to create climate transition plans to bring their business model in line with the Paris Agreement. Taking action on preparing this climate transition plan will support compliance with both directives.

- Data granularity: Both policies will require a need for greater data granularity across many topics, including environmental data (GHG emissions, resource usage), supply chain data (impacts of operations) social data (employee information, human rights), and governance data (board composition, executive compensation, risk management). Companies should therefore assess their data collection tools and processes to ensure they can comply with both directives.

- Stakeholder engagement: Both policies require sustainability and other teams to engage with affected external stakeholders. This is necessary to collect information, assess risks, and further understand the impacts of company activities throughout the supply chain.

In a nutshell, directors and officers should look for ways to streamline activities between the two directives. For instance, the double materiality assessment can serve as a starting point for identifying potential risks that should be included in the company’s due diligence procedures.

Differences in preparation for CSRD and CSDDD

Because of the differences in scope and focus of each directive, there will also be differences in preparation.

Since the focus of CSRD is on sustainability reporting, sustainability teams will need to prioritise ESG data collection and communication of these data points. As part of embedding sustainability into finance, this involves collecting more granular environmental, social, and governance data, prioritising this data, identifying reporting needs, and establishing company procedures for future data collection and reporting.

As an example, Maarten de Haan, Senior Manager of Global Environmental Sustainability at Kraft Heinz, has shared how the Double Materiality Assessment helped them determine which reporting tools they need. The assessment, according to de Haan, has given the company a better understanding of their reporting needs – making it clear they need sophisticated tools given the complexity and scope of their operations. After defining business requirements, they have vetted various reporting solutions and will pick one winning provider.

The data collection in preparation for the CSRD will also equip companies to implement the necessary due diligence procedures mandated by the CSS3D. However, companies subject to the CS3D will need to go beyond this to develop and integrate due diligence policies, grievance mechanisms, and more to ensure ongoing monitoring and compliance.

Companies that have already been implementing the advised due diligence procedures may need minimal preparation. IKEA, for example, has been focusing on due diligence for quite some time, establishing their supplier code of conduct IWAY in 2000. IWAY established comprehensive standards in several key areas of their business, specifying the code of conduct for suppliers in worker housing, animal welfare, ocean transport, and several additional areas.

In short, companies that have been following the OECD Guidelines for Multinational Enterprises could already be far along with their CS3D preparation.

How traceability solutions help with CSRD and CS3D compliance

To comply with these directives, directors and officers will need to analyse whether their existing traceability solutions are up to the challenge. Specifically, they should assess whether their existing solutions can collect the granular level of data they need to identify relevant human rights and environmental risks, impacts, and opportunities.

Traceability solutions that incorporate decentralised blockchain technology can provide companies with the supply chain visibility they need while keeping data privacy safe.

Circularise, for example, supports companies with complex chains with traceability software including Digital Product Passports and MassBalancer to collect data, generate proof of sustainable practices, and manage these sustainable practices. To highlight just a few of the many applications:

- Environmental impact tracking: A company can use Digital Product Passports to track the carbon footprint of a product, from raw material extraction to product disposal and build out an accurate life cycle assessment.

- Showcasing circularity: Companies can demonstrate steps toward circularity through Digital Product Passports that facilitate more effective end-of-life processing and recycling, for example for electric vehicle manufacturers needing to minimise the environmental impact of their batteries.

- Biofuel reporting: MassBalancer, Circularise’s mass balance solution and bookkeeping software, allows companies in industries like chemicals, plastics, and feedstock to easily report on the percentage of biofuels they use in their products and comply with certification schemes such as ISCC PLUS and ISCC EU.

- Human rights monitoring and due diligence: Digital Product Passports can provide necessary data and due diligence for human rights issues like labour conditions and hazardous waste disposal.

- Conflict mineral compliance: Digital Product Passports can help companies ensure they are sourcing minerals from responsible sources and avoiding minerals from conflict zones.

The CSRD and CSDDD incorporate these applications and many more, highlighting how sophisticated traceability solutions can transform companies’ sustainability reporting and management.

Ultimately, supply chain traceability partners like Circularise can help companies go far beyond compliance, enabling them to build their strategic competitive advantage through streamlined operations and sophisticated sustainability practices.

Conclusion

It’s never too soon to begin preparing for these directives. It’s up to directors and officers across sustainability, finance, procurement, and human resources to understand the implications of these directives for their departments, collaborate with their internal leaders, and ensure their departments begin preparing in time.

Given how detailed and comprehensive both directives are, it’s understandable that chief sustainability officers and other leaders might be feeling overwhelmed by the workload. Now is the time to shore up resources and build an external support team to assist with preparation, reporting, and due diligence. After all, these new directives are a clear sign that sustainability reporting and due diligence are the future and can’t be ignored.

As the leading sustainability traceability partner for companies in industries with complex supply chains like automotive, batteries, plastics, and metals, the Circularise team are here to help.

Circularise is the leading software platform that provides end-to-end traceability for complex industrial supply chains. We offer two traceability solutions: MassBalancer to automate mass balance bookkeeping and Digital Product Passports for end-to-end batch traceability.

Reach out to us to discuss how we can support you with supply chain traceability and sustainability compliance.

.png)