.avif)

With the Corporate Sustainability Reporting Directive (CSRD) in force, large EU firms are digging deep into their sustainability data. One of the first steps in CSRD compliance? The double materiality assessment — a process companies use to identify relevant topics for their sustainability reporting.

This dual approach to materiality is new for most companies. While many firms have used single materiality in past financial and sustainability reporting, double materiality requires companies to consider sustainability from two perspectives.

EFRAG, the organisation behind the CSRD’s sustainability standards, have published requirements and guidance for the assessment, but the language is complex, and best practices are still being developed. As a result, sustainability teams are eager to find additional guidance and examples.

To support you on CSRD compliance, here we’ll review the basics of the double materiality assessment, highlights from EFRAG’s implementation guidance, pitfalls to avoid, and finally, an example of the assessment in action.

What is double materiality?

“Materiality” is an important concept in the world of financial and sustainability reporting.

In finance, traditional materiality considers external issues that could affect the company’s financial performance. However, sustainability reporting typically focuses on impact materiality — ways a company impacts people and the environment.

Double materiality combines these two perspectives, considering materiality from both a financial and impact point of view. This means a double materiality approach considers the ways society and environment affect a company’s performance, as well as the ways that company impacts the environment and society. With this approach, a sustainability topic would be “material” if it is important from either perspective.

This is also referred to as an “in-side out” (impact materiality) vs an “outside-in” (financial) perspective.

Double Materiality: CSRD’s reporting filter

The double materiality assessment is like a filter for CSRD sustainability reporting. In order to determine which of the European Sustainability Reporting Standards (ESRS) companies must include in their sustainability reporting, teams must follow a systematic process to identify and prioritise related impacts, risks, and opportunities.

The assessment presents both challenges and opportunities: Since it’s a new and more demanding process, compliance with this approach requires time, resources, and adaptation. At the same time, companies that can quickly adapt to these new requirements could be seen by the public, investors, and stakeholders as industry leaders, solidifying their competitive advantage.

Below, we’ve outlined the essentials of the assessment to get you started.

Designing your double materiality assessment

EFRAG gives companies the freedom to design their own assessment process, as long as they meet several specific requirements. These requirements include:

- Using the issues listed in ESRS 1: general disclosures as the basis for the assessment

- Determining impact and financial materiality based on a scoring and threshold system

- Assessing financial materiality on a short and long-term horizon

- Using quantitative and qualitative data to support conclusions

- Disclosing the assessment process in reporting

Since the assessment is quite comprehensive, you will need input from departments across the organisation, including sustainability, finance, operations, HR, procurement, and others.

Sustainability matters to assess

The main sustainability topics to assess in the materiality assessment are the topics in appendix A of the ESRS 1: General disclosures.

This list includes three layers of sustainability matters:

- Topics (i.e. biodiversity and ecosystems)

- Sub-topics (i.e. direct impact drivers of biodiversity loss)

- and sub-sub topics (i.e. land-use change)

The list included in the ESRS should form the basis of the assessment, but companies shouldn’t limit themselves to this list and also consider company-specific topics or issues that have come up in past reporting.

How do impacts, risks, and opportunities relate?

Another core concept of the double materiality assessment is impacts, risks, and opportunities.

Impact refers to an impact arising from a sustainability issue, which could be either positive or negative. Companies must also consider risks and opportunities that arise from impacts and quantify their financial effects.

As an example, in their 2023 reporting, Unilever Group identified a number of impacts, risks, and opportunities related to climate change:

- One impact of climate change would be reduced crop output due to prolonged high temperatures and declining soil productivity

- This would likely result in the risk of higher raw material prices

- Climate-related issues would also result in relevant financial opportunities for Unilever, such as the growth in demand for plant-based or lab-grown foods

Although Unilever completed this report before its double materiality assessment, it’s a good example of how double materiality works in practice, and how impacts can lead to risks and opportunities.

Scoring and setting thresholds

In the assessment, companies must score the severity of actual and potential impacts and use appropriate thresholds to determine which impacts are material.

From an impact materiality perspective, teams should use evidence, past assessments, and results from stakeholder engagement to score relevant impacts. For “actual” material impacts, there are three criteria for scoring:

- Scale: how grave (or beneficial) the impact is to people and the planet

- Scope: how widespread the impact is

- Remediability: whether a negative impact can be reversed or fixed

When dealing with potential impacts (either negative or positive), teams need to factor in the impact’s likelihood and the relevant time horizon.

From a financial materiality perspective, teams need to score impacts and rank financial impacts based on:

- Time horizon: whether the company will experience the impact in the short or mid/ long term

- Size: the overall quantitative value of the financial impact

Companies should consider how the financial and material impacts interact. One way they can facilitate this process in their reporting is by creating a materiality matrix. This could show impact materiality on one axis, and financial materiality on the other, such as in the below simplified example.

Any issues in the top right would represent the highest-priority areas for the company from both a financial and impact perspective, but other topics could still be material if they are important from one perspective.

Using evidence and data in the assessment

According to EFRAG, companies can use both quantitative and qualitative data to assess issues. Supply chain data, scientific consensus, and stakeholder feedback should all come into play.

While performing the assessment, it’s wise to use your findings to assess whether your sustainability data, supply chain traceability tools, and reporting processes suit your needs for CSRD compliance.

By assessing the sustainability topics throughout your entire value chain in more detail, you may uncover gaps in data you need suppliers to provide. You could then, for example, implement digital passport products to provide product and material visibility throughout the entire value chain, without compromising sensitive data.

The granularity of data you’ll need for final reporting will depend on whether the topic is material, and which subtopics are material — both of which will be clear after the assessment.

A four-step approach to tackling the double materiality assessment

EFRAG provide a four-step example of how companies can complete the assessment in their implementation guidance, which we will summarise here.

Step 1: Understand the sustainability context of your company

The first step in this approach is to understand the bigger picture of your company’s value chain. This means defining the company’s business activities and business relationships so you can more accurately identify relevant impacts.

In this stage you can also define the various groups of stakeholders affected by your company, and outline how you currently engage with them about impacts. It’s also helpful to consider any other contextual information, like current regulatory environments.

Step 2: Identify the actual and potential impacts, risks and opportunities related to sustainability matters

The next step is to create a longlist of all the areas you need to assess. This includes all potential impacts, risks, and opportunities you need to consider further. As we’ve said, this list should use the topics in the ESRS 1: general disclosures as your basis, but should also include any company-specific areas.

If relevant, you can also use your GRI assessment outcome as a basis and cross-reference with the ESRS list, since they are closely aligned.

Step 3. Assess & determine the material IROs related to sustainability matters

The next step in EFRAG’s possible approach is to determine your criteria for assessing materiality, score, and thresholds.

While considering the scope and severity of your impacts, it’s important to use scientific consensus and relevant stakeholder engagement to inform which risks are most likely and could be the most severe.

Once you set your thresholds and complete scoring for financial and impact materiality, you can identify your material topics and sub-topics.

As you determine the relevant sustainability matters for your company, you’ll then need to determine the specific data points that need to be disclosed in line with the ESRS.

Step 4: Using the double materiality assessment in the reporting process

The final step in EFRAG’s approach is to prepare your assessment conclusions for your reporting.

As part of the sustainability statement in your management report, you’ll need to disclose the process your company used to identify and assess the material impacts, risks and opportunities. You must also describe how they interact with your strategy and business model.

And finally, once you have your material topics identified, your teams can move onto setting up the data and reporting systems they’ll need to report on the financial year.

Pitfalls to avoid when completing the double materiality assessment

So far, we’ve discussed what to do when completing the double materiality assessment. What are some of the mistakes to avoid?

Irrelevant stakeholder engagement

ESRS advisors have called out some corporations for their stakeholder engagement process. For example, one well-known electronics company was criticised for asking the public questions that would be better answered through scientific consensus.

The solution here is to think strategically about stakeholder engagement and which types of questions stakeholders are best suited to answer.

Seeing the double materiality assessment as a one-time exercise

Another pitfall to avoid is seeing the double materiality assessment as a one-off, tick-box exercise. Companies need to revisit their material topics each year, unless there are no notable changes. This is because the process is not static and will continue to evolve as the company, regulatory environment, and sustainability context evolve. This means it’s best to set yourself up for repeat success, doing the best job you can today while knowing you can improve each year.

Inconsistent scoping and threshold setting

Flimsy scoping and threshold setting can lead to gaps or miscalculations in the assessment. This can arise when different divisions and departments score topics independently, without enough context or a clear set of criteria.

For example, when evaluating risks, the North American division of a company might score circular economy risks as a three, due to the more lenient regulatory environment. Meanwhile, a European division might score this as a four, due to more stringent laws. Equipping teams with context and data will help set consistent thresholds that can accurately material issues from a global perspective.

Not considering both short-term and long-term materiality

The CSRD emphasises the importance of considering both short- and long-term impacts. This means companies need to balance these two in their assessment, especially when evaluating their own priorities and input from stakeholder engagement, which could be influenced by present bias.

Consulting scientific consensus and bodies like Science-Based Targets initiative (SBTi) can help companies more accurately evaluate longer-term impacts, for example through climate scenarios as part of ESRS E1 on climate change.

Assuming climate change is immaterial

Speaking of ESRS E1: climate change, it’s one of the more comprehensive topics companies have to assess. But given the scope and nature of climate change, most companies should find it material. If, after going through your assessment you find it isn’t material, there is likely an issue with your scoring and thresholds.

Unlike the other ESRS topics, for climate change, companies must submit a “negative materiality assessment” if they don’t deem it material in their assessment.

Double materiality assessment example

To date, few companies have published their double materiality assessments. And some of those published are not necessarily examples to follow.

However, we identified a 2023 double materiality assessment from Norwegian biorefinery Borregaard, a well-constructed assessment that other companies can use as inspiration. Here are a few of the points teams can learn from:

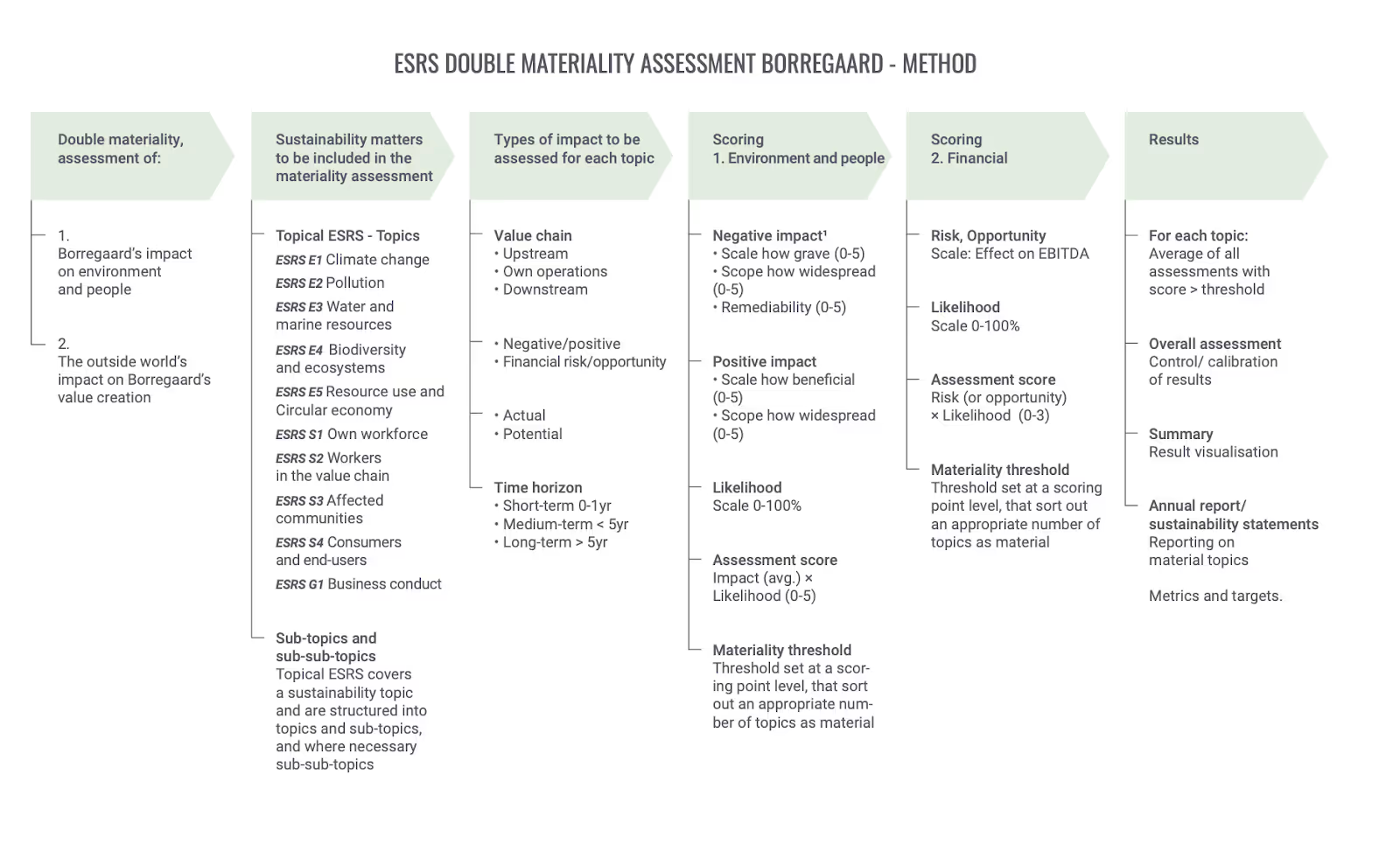

Process & method

First off, Borregaard describes the process they used to conduct their assessment, and how their existing risk analyses and due diligence processes informed the assessment.

While describing the process they used, Borregaard discusses the sustainability topics included in the assessment, the types of impacts they assessed, scoring, thresholds, and how they interpreted results.

Value mapping and stakeholder engagement

In the next section Borregaard provides an overview of their value mapping exercise, focusing mainly on the six stakeholder groups they identified. They also detail the 12 topics these stakeholder groups identified as important, providing insights into their stakeholders’ specific concerns and responses to these concerns.

Scoring

Borregaard also provides transparent but high-level information about how they scored impact and financial materiality.

As part of this process they took into account scale, scope, and remediability of material impacts, and analysed the positive and negative impacts upstream, downstream, and in their own operations. They also provide insights into their financial materiality scoring criteria.

While they present this information clearly, Borregaard could potentially provide more insights into how they assessed likelihood, magnitude, and nature of the effects in line with ESRS 2: general disclosures.

Results

The Borregaard report clearly showcase the topics and sub-topics that are material from both an impact and financial perspective, indicating the relative importance of each topic. They determined “direct impact drivers of biodiversity loss” under “biodiversity and ecosystems” was the most important impact topic from an impact perspective, and climate change was determined to be most important from a financial perspective.

After reporting their results, they provided additional detail on the sustainability information they will include in their reporting, and how they will use this information to address impacts, risks, and opportunities in these areas.

Compared to some of the other assessments currently published, Borregaard’s double materiality assessment is thorough, and appears to follow the guidelines for completing the assessment.

Along with reading and understanding the legislation and EFRAG’s implementation guidance, companies looking for a place to start can reference existing reports, such as Borregaard’s, for more insights into the process and work involved.

Conclusion

There is no doubt that the double materiality assessment is a complex process with many moving parts. Companies subject to the CSRD must now think about impact in a deeper, more holistic, and more systematic way. Since the double materiality assessment is one of the first steps of CSRD compliance, companies must prioritise this large task, especially firms that must report in 2025 and 2026.

At the same time, companies will benefit from seeing the double materiality assessment process as not just a tick box exercise, but also an invaluable tool to strengthen company reputation, operations, and finances in both the short- and long-term.

While there are many pieces to put in place, data will be a key driver in each stage of compliance. Life cycle assessments and carbon footprinting will be invaluable for the assessment, and companies may need new supply chain traceability tools for more granular sustainability reporting.

Circularise can help companies meet their data needs as part of CSRD compliance. No matter the sustainability topic, the Circularise team can help you identify gaps in your data and implement solutions for supply chain traceability and a smoother, more reliable double materiality assessment.

Circularise is the leading software platform that provides end-to-end traceability for complex industrial supply chains. We offer two traceability solutions: MassBalancer to automate mass balance bookkeeping and Digital Product Passports for end-to-end batch traceability.

Reach out to us to discuss how we can support you with supply chain traceability and sustainability compliance.